The landscape of retail fraud has undergone a profound transformation, moving beyond isolated acts of deception to coalesce into a sophisticated, commercialized ecosystem. What was once the domain of opportunistic individuals has evolved into a structured underground economy where illicit methods and services for exploiting consumer return policies and payment systems are actively developed, packaged, and traded like legitimate digital commodities. This insidious market leverages vulnerabilities in customer-centric business processes, enabling fraudsters to systematically extract value from major retailers and financial platforms, posing a significant and escalating threat to global commerce.

The Genesis of an Illicit Economy

Historically, refund fraud primarily manifested as isolated incidents, often stemming from individual attempts to circumvent return policies. However, recent analyses of clandestine online forums and darknet marketplaces reveal a stark evolution. Researchers examining thousands of digital artifacts from these communities have uncovered a thriving marketplace where actors openly market "refund methods," comprehensive tutorials, and even operational services. These offerings are meticulously designed to exploit the refund workflows of prominent e-commerce giants and payment processors. Crucially, this new wave of fraud often bypasses traditional cyberattack vectors like malware or complex hacking. Instead, it weaponizes a far more accessible resource: intimate knowledge of customer service protocols, payment dispute mechanisms, and the operational nuances of large-scale retail. By manipulating procedures originally instituted to safeguard consumers, fraudsters have successfully engineered a scalable illicit business model, transforming established refund policies into a vulnerability.

Dissecting the Mechanics of Deception

At its core, refund fraud refers to instances where individuals illicitly obtain cash, replacement products, or store credit from companies without genuinely returning merchandise or services. This often falls under the umbrella of social engineering, exploiting human trust and procedural gaps, though it can sometimes intersect with financial fraud or account takeover techniques. Threat actors meticulously study and exploit return guarantees, chargeback systems, and customer-service escalation paths to coerce companies into issuing refunds, even for legitimately purchased items.

Several common tactics underpin this fraudulent activity:

- Item Not Received (INR): Perpetrators falsely claim a delivered package never arrived, pressuring the retailer or shipping carrier for a refund or replacement.

- Partial Refund Scams: Fraudsters claim only a portion of their order was received or that some items were damaged, seeking a partial reimbursement while retaining all goods.

- Empty Box Scheme: The fraudster returns a package containing only air or an irrelevant, valueless item, claiming to have returned the correct, high-value product.

- Swap Scam: A legitimate, often expensive item is purchased and then returned with a cheaper, identical-looking counterfeit or a broken version of the original.

- Damaged Item Claim: Fraudsters intentionally damage an item they received and then claim it arrived in that condition to receive a refund or replacement.

- Chargeback Abuse (Friendly Fraud): While technically distinct, this often overlaps. Consumers dispute legitimate charges with their bank, claiming unauthorized transactions or non-delivery, leading to a chargeback that forces the merchant to refund the money and often pay a fee.

The prevalence of these schemes is facilitated by a prevalent retail philosophy: prioritizing rapid customer issue resolution and minimizing friction in the returns process. This customer-centric approach, while beneficial for legitimate consumers, inadvertently creates exploitable pathways for those who understand internal operational mechanics.

The Staggering Economic Toll on Retail

The financial implications of this evolving fraud landscape are immense, imposing a multi-billion dollar burden on the global retail sector. In today’s highly competitive consumer markets, customer expectations for flexible return policies are sky-high. Data from the National Retail Federation (NRF) and retail technology firm Narvar indicates that approximately 76% of consumers consider free returns a significant factor in their purchasing decisions. This market dynamic severely constrains retailers’ ability to tighten refund policies without alienating their legitimate customer base, thereby inadvertently creating a fertile ground for refund fraud to flourish.

Refund fraud has consequently emerged as one of the most financially damaging forms of e-commerce malfeasance. According to research by the NRF and Appriss Retail, retailers processed an estimated $685 billion worth of merchandise returns in 2024, representing about 13% of total retail sales. A staggering $103 billion, or roughly 15% of these returns, were attributed to fraudulent activity. The financial impact extends beyond direct losses; additional research suggests that for every dollar lost to fraud, businesses incur an additional four dollars in operational costs, encompassing investigative efforts, dispute resolution, and administrative overhead. This exponential cost multiplier underscores the profound economic drain on businesses, ultimately contributing to higher prices for all consumers.

Inside the Fraud Black Markets: A Structured Ecosystem

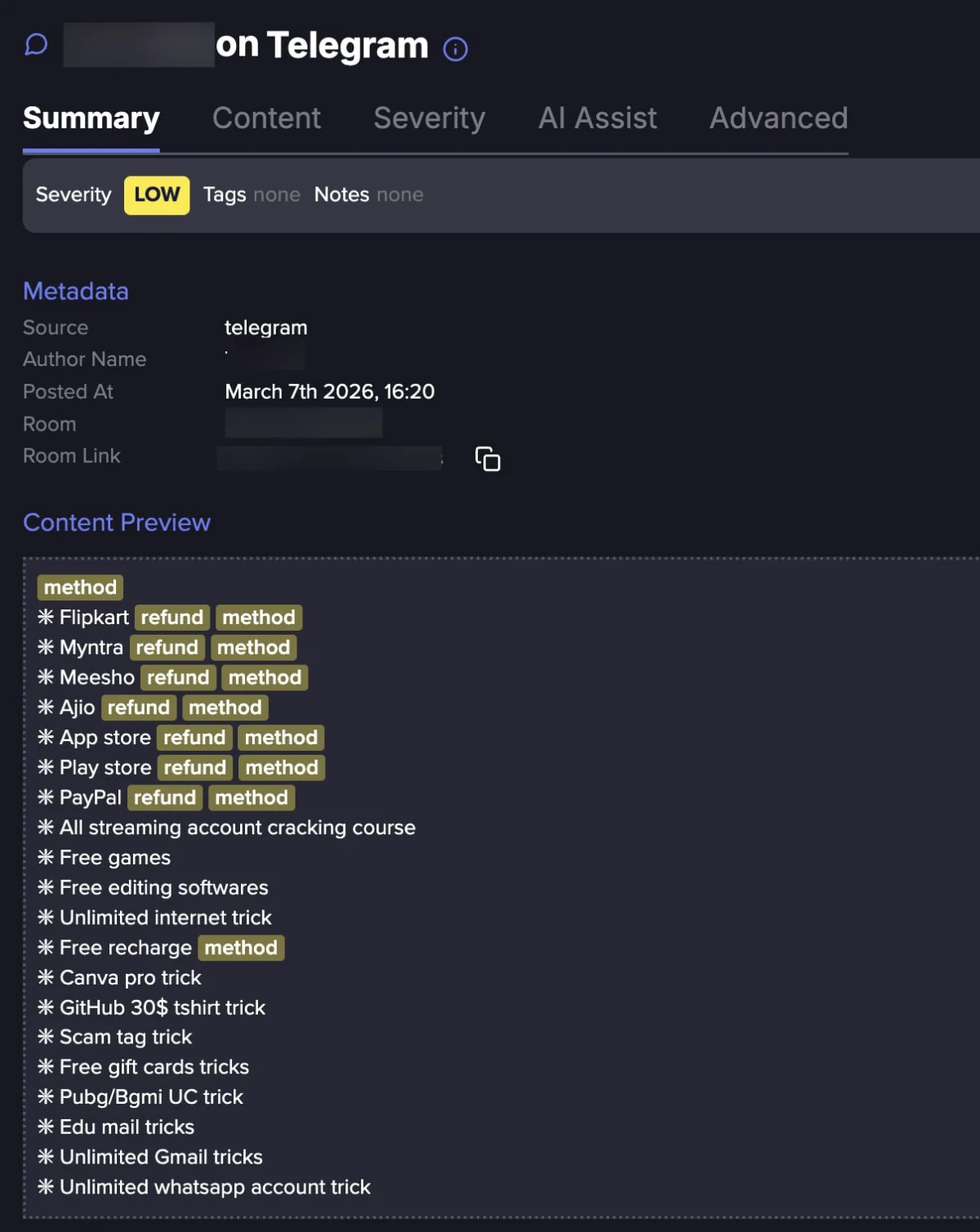

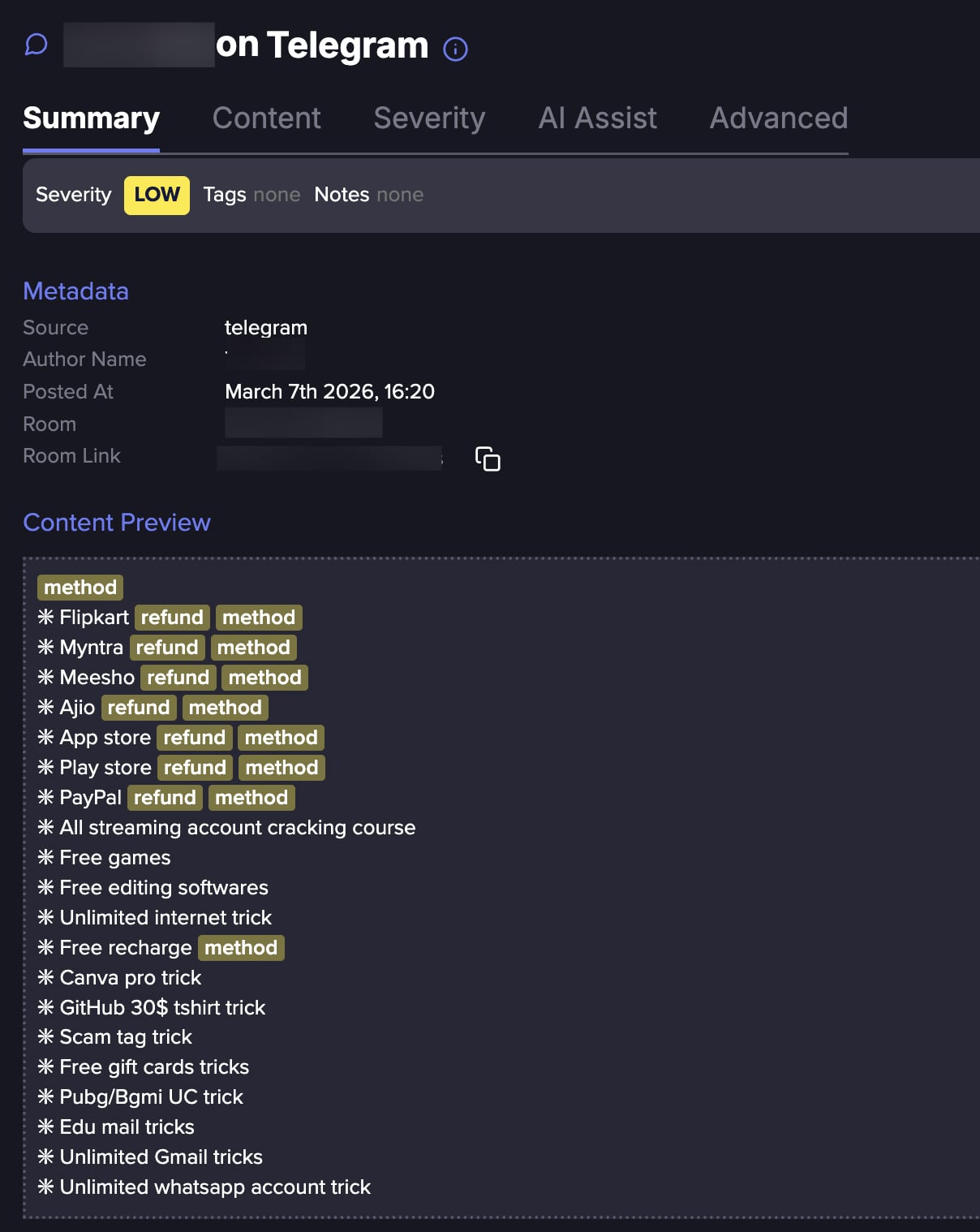

The sophistication of this illicit activity is best understood by examining its operational core: the fraud-focused black markets. Initial attempts to survey these digital undergrounds for "refund" related posts yielded tens of millions of results, highlighting the sheer volume of discussion. Refining the search to specifically target "refund" in conjunction with terms like "method" or "tutorial" significantly narrowed the scope, revealing millions of relevant posts, with hundreds of thousands appearing monthly.

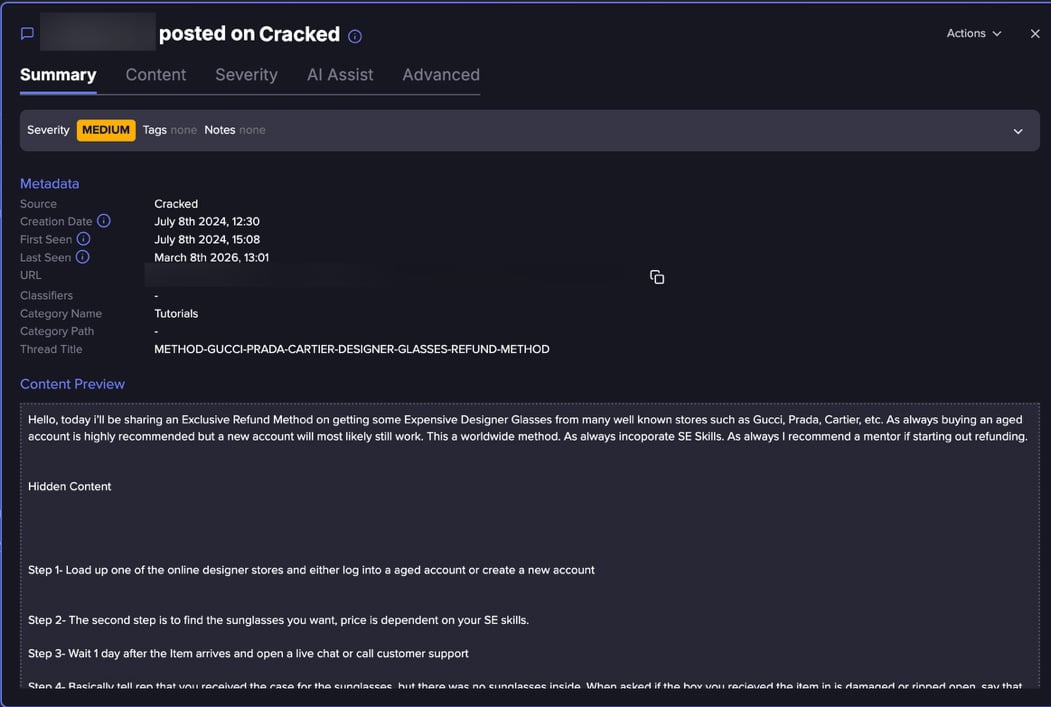

A detailed sampling of nearly 4,000 posts provided critical insights into how refund fraud is being operationalized. The analysis unveiled a highly commercialized ecosystem where actors advertise illicit techniques in a manner strikingly similar to legitimate digital content platforms. A "tutorial" in this context effectively functions as an "online course," providing step-by-step instructions on how to defraud businesses. The high incidence of duplicate messages (over 1,600 unique messages out of nearly 3,700 posts) suggests a deliberate strategy by sellers to maximize visibility and reach across multiple communities.

These advertisements predominantly promote "refund methods," detailed "tutorials," "step-by-step guides," and even "vendor refund services." The pricing structure is indicative of a market designed for broad accessibility, with tutorials typically ranging from $50 to $300. This low entry barrier attracts both seasoned fraudsters and novices seeking an inexpensive gateway into illicit activities. Furthermore, a burgeoning "refund fraud as a service" (RaaS) model has emerged, mirroring legitimate SaaS trends. In this arrangement, specialized operators perform the refund manipulation on behalf of customers, typically earning a commission of 30% to 50% of the refunded value. This service-oriented model allows fraudsters to scale operations efficiently, applying their mastered techniques across numerous cases without significant per-case time investment.

Targeting High-Value Platforms and Global Reach

The analysis of underground communications consistently reveals a focus on several major consumer platforms and payment services. Amazon, PayPal, Apple, eBay, Walmart, Best Buy, various delivery platforms, and prominent digital payment services are frequently referenced as prime targets. These entities share common characteristics that render them particularly attractive to fraudsters:

- High Transaction Volume: Their sheer scale means a greater number of potential targets and transactions to exploit.

- Established Refund Policies: Robust, often consumer-friendly, refund and dispute resolution systems are inherent to their business models, providing clear pathways for manipulation.

- Global Reach and Diverse Product Lines: Operating across numerous geographies and offering a vast array of products (from physical goods to digital content) provides multiple points of entry and varying levels of security scrutiny.

- Customer-Centric Approaches: Their emphasis on customer satisfaction and frictionless experiences often translates into expedited refund processes, which can be exploited by those who understand how to trigger these fast-track mechanisms.

The specific vulnerabilities of these platforms can also vary. For instance, Amazon’s extensive third-party seller marketplace can present unique opportunities for fraudsters to target less sophisticated vendors. PayPal’s dispute resolution process, while designed to protect buyers, can be abused by those filing fraudulent claims. Apple’s ecosystem, with its blend of physical products and digital services, offers diverse vectors for exploitation.

Lowering the Entry Barrier: The Democratization of Fraud

Perhaps one of the most critical insights from recent research is the standardization and productization of refund fraud techniques. By transforming complex operational knowledge into accessible tutorials and step-by-step guides, underground sellers have significantly lowered the entry barrier. This enables individuals with minimal technical expertise or prior experience to actively participate in sophisticated fraud schemes.

Unlike many other forms of cybercrime that demand advanced technical prowess, refund fraud often operates in a "gray area" between legitimate consumer behavior and deliberate deception. Individuals purchasing these tutorials may initially perceive their actions as relatively harmless, a minor exploit of corporate policy. However, exposure to these communities and methods can gradually draw them deeper into more organized and malicious forms of financial crime.

The emergence of "refund fraud as a service" further democratizes this illicit activity. In this model, a customer acquires a product and then collaborates with a professional threat actor who executes the refund manipulation process, with profits subsequently split. The incentives are clear: "customers" gain access to goods or cash without paying, guided by experts, while fraudsters scale their operations efficiently, leveraging their expertise across numerous transactions. This mirrors the "as-a-service" trend seen across other cybercrime markets, such as ransomware or phishing kits. However, in refund fraud, the "product" is not a piece of software but procedural knowledge—guidance on how to manipulate existing systems and exploit operational gaps.

Despite not requiring advanced technical capabilities, the cumulative impact of refund fraud on businesses can be as devastating as more technically sophisticated cybercrimes like malware campaigns or ransomware attacks. The growing underground market for these tutorials and services vividly illustrates how modern cybercrime increasingly targets not only technological vulnerabilities but also the inherent business logic and operational processes of online platforms.

Strategic Responses and Future Outlook

For e-commerce companies, retailers, payment providers, and any organization operating digital services, these developments underscore the imperative of maintaining robust threat intelligence capabilities. A proactive understanding of emerging fraud techniques is paramount for staying ahead of evolving threats. This involves continuously monitoring dark web forums, analyzing attack patterns, and sharing intelligence across the industry.

Effective mitigation strategies must be multi-faceted:

- Enhanced Threat Intelligence: Moving beyond internal data to integrate external intelligence on new methodologies, targeted brands, and emerging fraud-as-a-service offerings.

- Advanced Analytics and AI/ML: Deploying sophisticated algorithms to detect anomalous return patterns, identify suspicious account behavior, and flag potential fraud indicators in real-time.

- Strengthened Authentication: Implementing multi-factor authentication for high-value transactions or sensitive account actions, even for returns.

- Robust Internal Processes and Employee Training: Regularly updating customer service protocols and providing comprehensive training to employees to recognize social engineering tactics and suspicious refund requests.

- Cross-Industry Collaboration: Fostering partnerships and information-sharing initiatives among retailers, payment processors, and law enforcement agencies to collectively combat organized fraud.

- Adaptive Policy Adjustments: Carefully re-evaluating return policies to strike a balance between customer convenience and fraud prevention, potentially introducing tiered return processes based on item value or customer history.

- Legal and Enforcement Action: Collaborating with law enforcement to identify and prosecute individuals and organized groups perpetrating refund fraud, sending a strong deterrent message.

The "Refund Fraud Economy" represents a significant challenge, demonstrating the ingenuity of malicious actors in exploiting the very systems designed to foster trust and convenience in digital commerce. As this illicit market continues to evolve, driven by accessibility and commercialization, the ongoing arms race between fraudsters and fraud prevention specialists will intensify. Success for businesses will depend on a proactive, intelligence-driven approach that combines technological defenses with a deep understanding of human psychology and operational vulnerabilities.