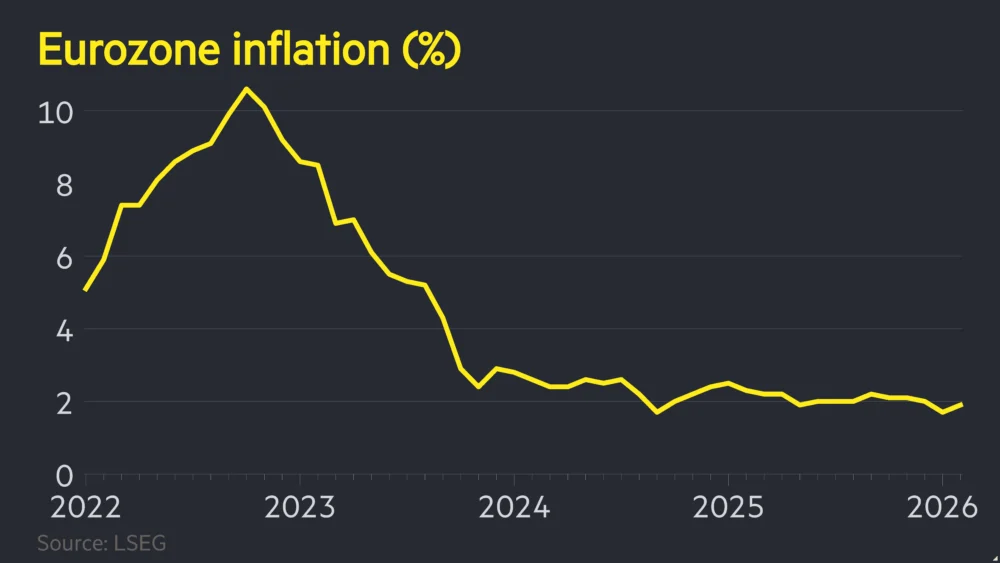

February witnessed an unexpected uptick in inflation across the Eurozone, reaching a concerning 1.9 percent, a development that deviates from the anticipated disinflationary trend and injects a new layer of complexity into the region’s economic outlook. This upward revision, exceeding market expectations and previous forecasts, suggests that the forces driving price increases remain more entrenched than previously understood, posing potential challenges for policymakers at the European Central Bank (ECB). The data indicates a need for a more nuanced understanding of the current inflationary environment, moving beyond simple assumptions of a steady decline and delving into the underlying dynamics that are contributing to this renewed price pressure.

The Eurozone’s inflation rate, a crucial barometer of economic health, has been a focal point for economists and central bankers alike for an extended period. Following a period of sustained elevated levels, a gradual deceleration was widely projected for the early months of 2024, fueled by factors such as easing energy costs and the anticipated impact of monetary policy tightening. However, the February figures have defied these predictions, prompting a re-evaluation of the prevailing economic narrative. This unexpected acceleration underscores the volatile nature of inflation and the interconnectedness of global economic factors that can swiftly alter domestic price trajectories.

Deeper Dive into the Inflationary Drivers

Several key factors are believed to be contributing to this surprising inflationary surge. While headline inflation, which includes volatile components like energy and food, has shown some moderation in certain categories, the underlying price pressures appear to be broadening. Core inflation, which excludes these more volatile items, is of particular concern to policymakers as it offers a clearer view of persistent inflationary trends. The latest data suggests that core inflation may be proving more resilient than anticipated, driven by a confluence of demand-side and supply-side pressures.

On the demand side, while consumer spending has faced headwinds from high interest rates, pockets of resilience may be emerging. Wage growth, though slowing in some sectors, continues to provide a degree of support to household incomes, enabling a sustained, albeit more cautious, level of consumption. Furthermore, the impact of fiscal stimulus measures implemented in various member states during recent economic shocks may still be filtering through the economy, contributing to aggregate demand.

Supply-side factors also remain a significant influence. While the acute supply chain disruptions witnessed during the pandemic have largely abated, certain sectors continue to experience elevated input costs. The cost of raw materials, although fluctuating, can still exert upward pressure on final goods prices. Moreover, geopolitical tensions and their impact on global trade routes and commodity markets introduce an element of uncertainty, capable of triggering localized or even broader supply shocks that translate into higher prices for businesses and consumers. The ongoing conflict in Eastern Europe, for instance, continues to cast a shadow over energy and agricultural markets, maintaining a baseline level of price volatility.

Sector-Specific Analysis and Emerging Trends

A granular examination of the inflation components reveals specific sectors where price increases are proving particularly persistent. Services inflation, often considered a bellwether for underlying domestic price pressures due to its closer link to wage costs, has shown notable strength. This is likely attributable to a tight labor market in certain service industries, leading to upward wage adjustments that are then passed on to consumers. Sectors such as hospitality, transportation, and personal care are exhibiting a greater tendency to reflect these higher labor costs in their pricing.

Conversely, the inflation rate for manufactured goods, excluding energy and food, has also shown a surprising resilience. While the initial shock of supply chain bottlenecks has eased, the cost of certain intermediate goods and the ongoing adaptation of production processes to new geopolitical realities continue to influence pricing strategies. The transition towards more sustainable and resilient supply chains, while a long-term positive, can entail upfront investment costs that may be reflected in product prices in the interim.

Energy prices, while having fallen from their peaks, remain a critical factor. Although the direct contribution to headline inflation may have moderated, their indirect impact on transportation costs and the production of a wide range of goods and services continues to be felt. Fluctuations in global oil and gas markets, influenced by production decisions by major oil-exporting nations and geopolitical events, can quickly alter the inflationary landscape.

Implications for the European Central Bank (ECB)

This unexpected rise in Eurozone inflation presents a significant challenge for the European Central Bank. The ECB has been engaged in a delicate balancing act, aiming to curb inflation without triggering a severe economic downturn. The current data suggests that the disinflationary process may be slower and more uneven than initially anticipated, potentially forcing the ECB to reconsider its monetary policy trajectory.

The central bank’s primary mandate is price stability, and the sustained deviation from its inflation target of 2 percent will undoubtedly be a cause for concern. While the ECB has indicated a willingness to consider interest rate cuts later in the year, this latest inflation data may temper such expectations or necessitate a more cautious approach. The persistence of inflation, particularly core inflation, could lead to a prolonged period of higher interest rates, which would continue to weigh on economic activity and investment.

Furthermore, the ECB faces the challenge of communicating its policy intentions effectively to markets and the public. Any perception of policy missteps or a lack of clarity could exacerbate inflationary expectations and undermine the central bank’s credibility. The decision-making process will likely involve a careful assessment of forward-looking indicators, the evolution of wage negotiations, and the ongoing impact of geopolitical developments on commodity prices and supply chains.

Economic Growth and Inflationary Pressures: A Complex Interplay

The relationship between economic growth and inflation is a perennial concern for policymakers. In the current Eurozone context, the surprising inflation data raises questions about the sustainability of economic recovery. While some economic indicators have shown signs of resilience, sustained higher inflation can erode purchasing power, dampen consumer confidence, and ultimately hinder growth prospects.

If inflation remains elevated, businesses may face increased operating costs, potentially impacting profitability and investment decisions. This, in turn, could lead to a slowdown in job creation or even job losses. The delicate balance between taming inflation and fostering robust economic growth will be a central theme in policy discussions throughout the coming months.

The impact of higher interest rates, a tool used to combat inflation, also needs careful consideration. While designed to cool demand, prolonged high rates can stifle investment and lead to a contraction in economic activity. The ECB will need to gauge the precise impact of its past rate hikes and determine whether further tightening, or a prolonged period of restrictive policy, is necessary to achieve its inflation objectives.

Geopolitical Factors and Future Outlook

Geopolitical developments continue to play a pivotal role in shaping the global and Eurozone economic landscape. The ongoing conflict in Ukraine, potential shifts in trade relations, and broader geopolitical realignments can all contribute to inflationary pressures through their impact on energy markets, commodity prices, and global supply chains. Any escalation or de-escalation of these tensions will have direct implications for inflation trends.

Looking ahead, the outlook for Eurozone inflation remains subject to considerable uncertainty. While some disinflationary forces are expected to persist, the unexpected acceleration in February suggests that the path back to the ECB’s target may be more complex than initially envisioned. Key factors to monitor will include the evolution of wage growth, the persistence of services inflation, the trajectory of energy prices, and the broader impact of geopolitical events.

The ECB will likely maintain a data-dependent approach, closely scrutinizing incoming economic figures to inform its policy decisions. The possibility of a prolonged period of elevated inflation cannot be entirely discounted, which would necessitate a more hawkish stance from the central bank. Conversely, if inflationary pressures begin to recede more rapidly than anticipated, the ECB may find room to begin easing monetary policy, thereby supporting economic growth. The coming months will be critical in determining the prevailing economic trajectory for the Eurozone.