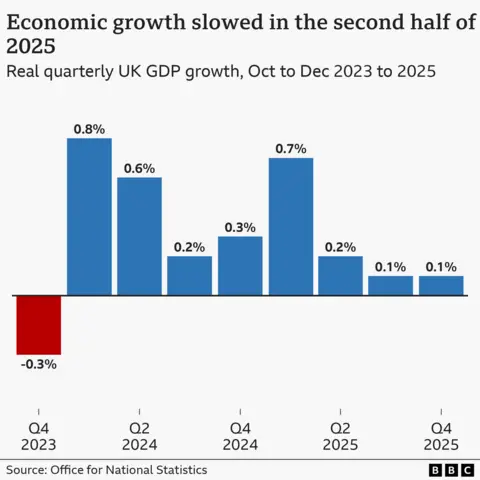

The United Kingdom’s economic expansion concluded 2025 on a decidedly cautious note, with official data revealing a modest 0.1% increase in Gross Domestic Product (GDP) during the final quarter, a figure that undershot market expectations and underscored persistent challenges within key sectors. This lukewarm performance for the October-December period cast a shadow over the government’s economic agenda and intensified scrutiny of the nation’s underlying growth potential as it transitions into the new year.

The Office for National Statistics (ONS), the country’s primary provider of independent statistics, highlighted that the critical services sector, which constitutes over 80% of the UK’s economic output, experienced an unprecedented period of stagnation, registering zero growth for the first time in more than two years. This flatlining of services activity was a significant concern, as the sector typically serves as the primary engine of British economic dynamism. The marginal overall GDP increment was primarily salvaged by a resilient, albeit limited, uptick in manufacturing output, which helped offset weaknesses elsewhere in the economy. Conversely, the construction industry endured its most challenging quarter in four years, signaling deeper structural issues within the built environment.

Analyzing the annual performance, the UK economy is estimated to have expanded by 1.3% across the entirety of 2025. While this represented a slight improvement over the 1.1% growth recorded in the preceding year, it conspicuously fell short of the 1.4% projection put forth by the Bank of England, indicating that the nation’s recovery trajectory was not as robust as anticipated by monetary authorities. This deviation from forecasts suggests that underlying economic headwinds were stronger or more persistent than initially modeled, challenging both fiscal and monetary policy frameworks.

A granular examination of the data reveals the nuanced landscape of the UK economy at year-end. The construction sector, a vital component of infrastructure development and employment, contracted by a notable 2.1% in the final quarter of 2025. This downturn was attributed to a dual impact: a reduction in essential repair and maintenance commissions, alongside a discernible slowdown in the initiation of new construction projects. The confluence of these factors points to a broader reticence in investment and development, potentially influenced by higher borrowing costs and a cautious outlook among developers and clients alike. The implications of such a sustained decline in construction activity extend beyond the sector itself, affecting supply chains, material suppliers, and the broader labor market.

Within the dominant services sector, the absence of aggregate growth masked a mixed performance across its various sub-components. Certain segments demonstrated commendable resilience and even growth, notably travel agencies, tour operators, and administrative support firms. The buoyancy in these areas might reflect a continued post-pandemic rebound in leisure and business travel, or an increased demand for outsourcing and operational efficiency solutions among businesses. However, these positive contributions were largely counteracted by a significant contraction of 1.1% in professional, scientific, and technical activities. This particular decline is noteworthy, as these high-value-added sectors are often indicators of business confidence and innovation. A downturn here could signal reduced corporate investment in research, development, consulting, and specialized services, reflecting a broader hesitancy in business expansion.

Several idiosyncratic factors also played a role in shaping the quarter’s economic narrative. The manufacturing sector received a specific boost from Jaguar Land Rover, which successfully brought its production capabilities back online following a major cyber-attack earlier in the year. This recovery provided a localized, yet significant, fillip to industrial output. However, this positive impact was partially overshadowed by a broader climate of economic uncertainty that preceded the November Budget announcement. Speculation regarding potential tax adjustments and fiscal policy shifts led many companies to defer or withhold planned investments, demonstrating the acute sensitivity of corporate decision-making to policy predictability. This "wait-and-see" approach, while rational for individual firms, can collectively dampen overall economic activity.

Liz McKeown, an economist at the ONS, succinctly summarized the prevailing sentiment, characterizing the overall economic picture as one of "subdued growth." This assessment resonates with the observations of external analysts. Ruth Gregory, Chief UK Economist at Capital Economics, described the growth figures as "disappointing," underscoring the enduring lack of significant economic momentum within Britain. These expert interpretations collectively paint a picture of an economy grappling with structural constraints and an absence of strong catalysts for accelerated expansion.

The economic data has naturally ignited a fervent political debate, given the Labour government’s explicit commitment to prioritizing economic growth since assuming power. Chancellor Rachel Reeves articulated a defense of the government’s economic strategy, asserting that their policy choices had established the necessary groundwork for the Bank of England to consider future interest rate reductions. She further contended that Britain’s economy, despite the recent figures, maintained its position as the fastest-growing European economy within the G7 group of leading industrialized nations. This comparison, while strategically deployed, often requires careful contextualization, as different nations may be at varying stages of their economic cycles and recovery from global shocks.

In stark contrast, Sir Mel Stride, the Shadow Chancellor, launched a robust critique, alleging that the Labour administration had "weakened our economy." He described the statistics as "disappointing" and indicative of a Downing Street and Treasury that had become complacent, "taken their eye off the ball." This political sparring highlights the high stakes associated with economic performance, particularly in the lead-up to future electoral contests. The Liberal Democrats echoed this criticism, contending that Chancellor Reeves’ initial two Budgets had effectively "killed off the economic recovery our country so desperately needs," pointing to a perceived failure of fiscal management.

Beyond the political rhetoric, business organizations voiced significant concerns. The British Chambers of Commerce (BCC) articulated that 2025 had been a year "marked by uncertainty and rising costs for firms across the country." Surveys conducted by the BCC consistently revealed that taxes and escalating inflation remained the paramount concerns for business leaders. This feedback underscores the tangible impact of fiscal policy on corporate operational costs and investment decisions. Specifically, many business executives have expressed persistent dissatisfaction with the increased tax burden, particularly the Chancellor’s decision to raise employer National Insurance contributions, which directly elevates the cost of hiring and retaining staff. This policy, intended to bolster public finances, has been perceived by many businesses as a disincentive to employment growth, especially for small and medium-sized enterprises (SMEs) operating on tighter margins.

The real-world ramifications of these macroeconomic trends are evident in the experiences of individual businesses. Nigel Day, who operates a heat pump installation business in Ipswich, provided a compelling case study. He reported that the prevailing uncertainty surrounding the November Budget had rendered his customer base hesitant to commit to significant expenditures. Furthermore, Day highlighted the direct impact of government policy on his operational choices. He explained that increases to the minimum wage, while beneficial for individual workers, had inadvertently made it economically unviable to employ younger, less experienced individuals simply as "an extra pair of hands." This cost pressure also forced his company to refrain from taking on apprentices, a decision with long-term implications for skills development and future workforce capacity within his industry. Day’s testimony illustrates the complex interplay between government policy, business viability, and employment dynamics at the microeconomic level.

Against this backdrop of modest growth and business apprehension, the Bank of England’s recent monetary policy decisions gained added significance. In the preceding week, the Monetary Policy Committee (MPC) opted to maintain interest rates at their current level, a decision reached after a narrowly divided vote. Concurrently, the Bank revised its forecast for economic growth in the upcoming year (2026) downwards to 0.9%, a reduction from its earlier prediction of 1.2%. Compounding this more pessimistic outlook, the Bank also increased its expectation for the unemployment rate, projecting it to rise from an initial forecast of 5% to 5.3%. These adjustments signal a cautious stance from the central bank, acknowledging persistent economic fragilities.

The Bank’s revised forecasts naturally fueled speculation regarding the timing of potential interest rate cuts. Rob Wood, Chief Economist at Pantheon Macroeconomics, suggested that the latest subdued growth figures would likely embolden those members of the MPC who advocate for a rate reduction, potentially leading to a cut as early as March. However, Wood also cautioned that any such move might represent the "last rate cut of the current cycle," implying that while short-term adjustments might be necessary, fundamental economic momentum might not warrant a sustained period of easing.

Conversely, Suren Thiru, Economics Director at the Institute of Chartered Accountants in England and Wales (ICAEW), expressed skepticism about an imminent rate cut in March. He posited that the marginal increase in economic output, however small, would provide policymakers with sufficient "comfort" to defer any rate reductions. This approach would allow the MPC to accumulate further evidence that inflationary pressures are definitively subsiding and are on a sustainable path towards the Bank’s target before committing to a shift in monetary stance. This divergence in expert opinion underscores the delicate balance the Bank of England must strike between supporting economic activity and ensuring price stability.

Looking ahead, the UK economy faces a complex array of challenges and opportunities. While the overall annual growth figure for 2025 indicated a modest expansion, the granular details of the fourth quarter performance highlight underlying fragilities, particularly in the critical services and construction sectors. The interplay between fiscal policy, monetary decisions, and global economic conditions will define the trajectory for 2026. The government’s ability to foster business confidence, encourage investment through stable and predictable policy, and address the cost-of-living pressures facing households will be crucial. Similarly, the Bank of England’s navigation of interest rate policy, balancing inflation control with support for economic activity, will remain under intense scrutiny. The path to robust, sustainable growth appears to be fraught with complexity, requiring judicious policymaking and adaptability from all economic actors.